Investment Team Voices Home Page

Investment Team Voices Home Page

CTSIX: Capitalizing on Fundamentally Driven Markets and Small Cap Catalysts

February 27, 2024

- After a multi-year period of macro-dominated markets and mega-cap leadership, we’re seeing a shift to an environment where fundamentals matter more and leadership has broadened.

- As investors have become more attentive to quality and company specifics, Calamos Timpani Small Cap Growth Fund has surpassed peers and the small-cap market overall.

- We see additional upside for the equity market and believe small cap growth stocks are set to gain momentum, supported by valuations, earnings growth, interest rate cuts, and the presidential election cycle; our team views these influences as the “icing on the cake” for its time-tested process.

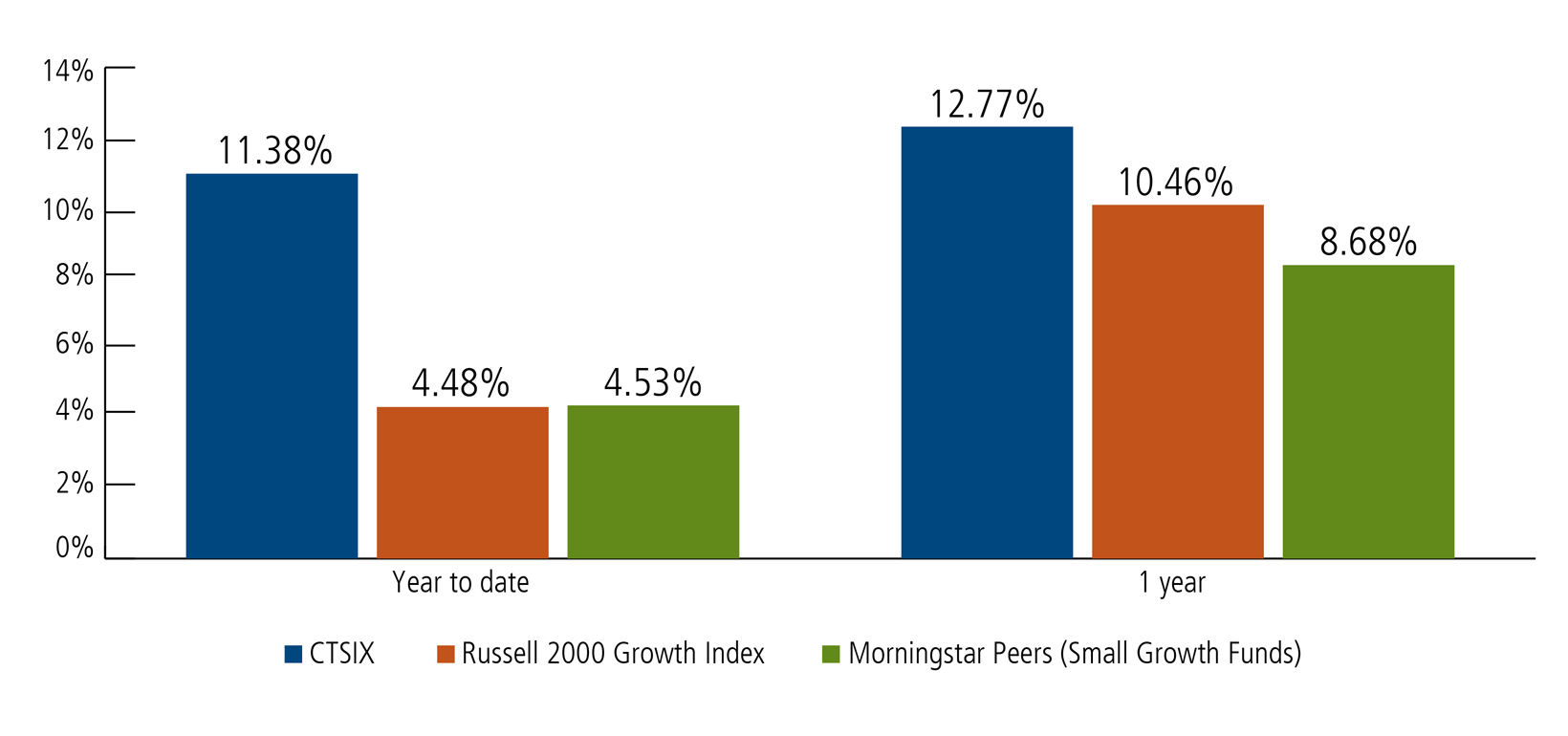

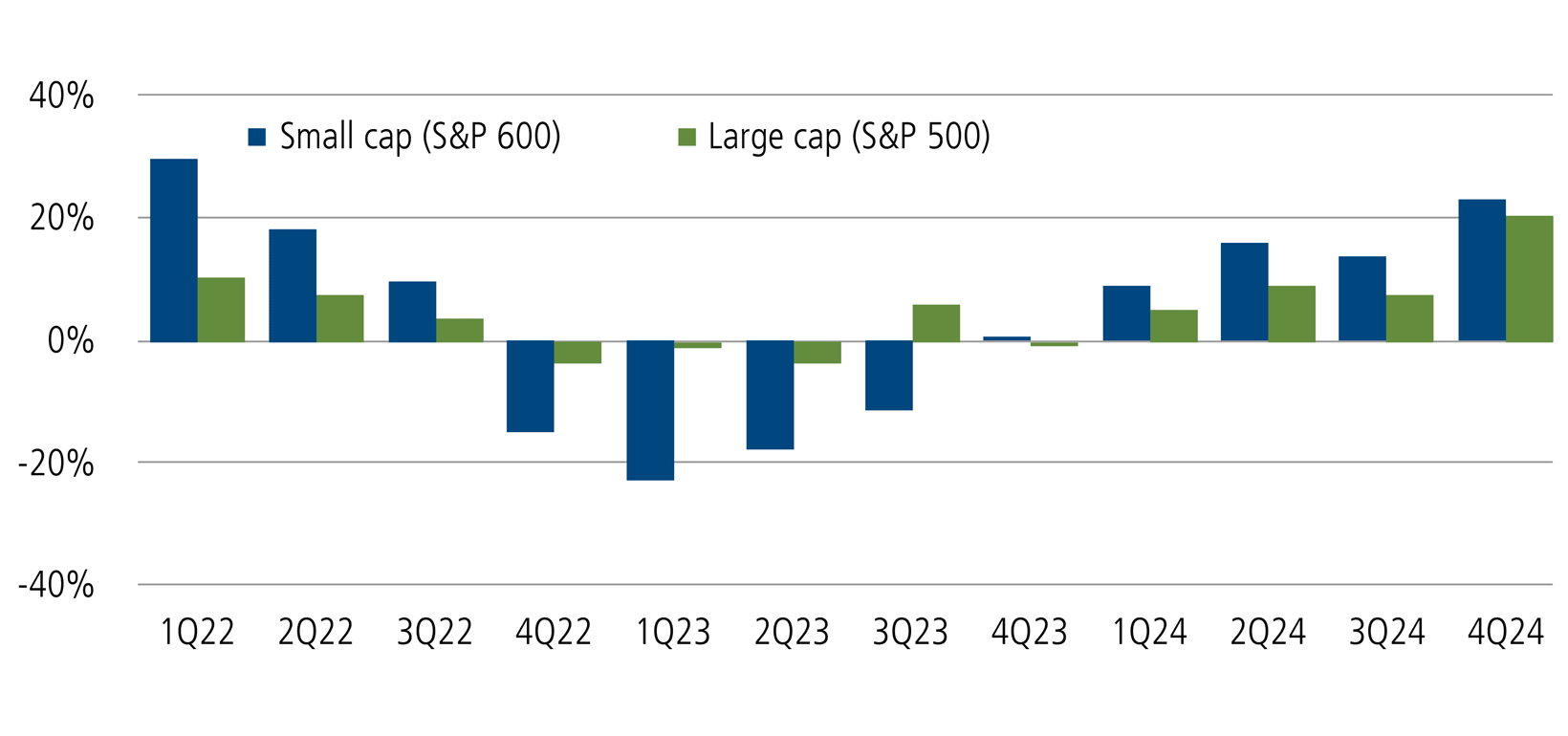

As fundamentals come back in favor, Calamos Timpani Small Cap Growth Fund has outperformed

Catalysts for small cap growth companies in 2024 … and beyond

- Rate cuts

- Earnings

- Valuations

Macro influences will—and should—always matter to the markets. However, over recent years, macro considerations have driven markets to an unusual degree. As investors tended to paint entire swaths of the market with broad brush strokes, many companies with strong fundamentals were overlooked. For example, even small companies with low debt came under pressure when interest rates rose, while enthusiasm about obesity treatment breakthroughs contributed to an at-times myopic view about the relative merits of companies in other parts of health care. In this environment, Calamos Timpani Small Cap Growth Fund’s high-conviction approach and emphasis on fast-growing companies with sustainable and underestimated growth potential came under pressure.

More recently, we’ve seen the macro grip on the markets weaken. As fundamentals become more important to investors, CTSIX’s focus on companies with sustainable, above-average growth prospects and strong stock momentum has been rewarded for both the year-to-date and one-year periods.

CTSIX has established a wide lead versus peers in 2024

Total returns as of 2/15/2024

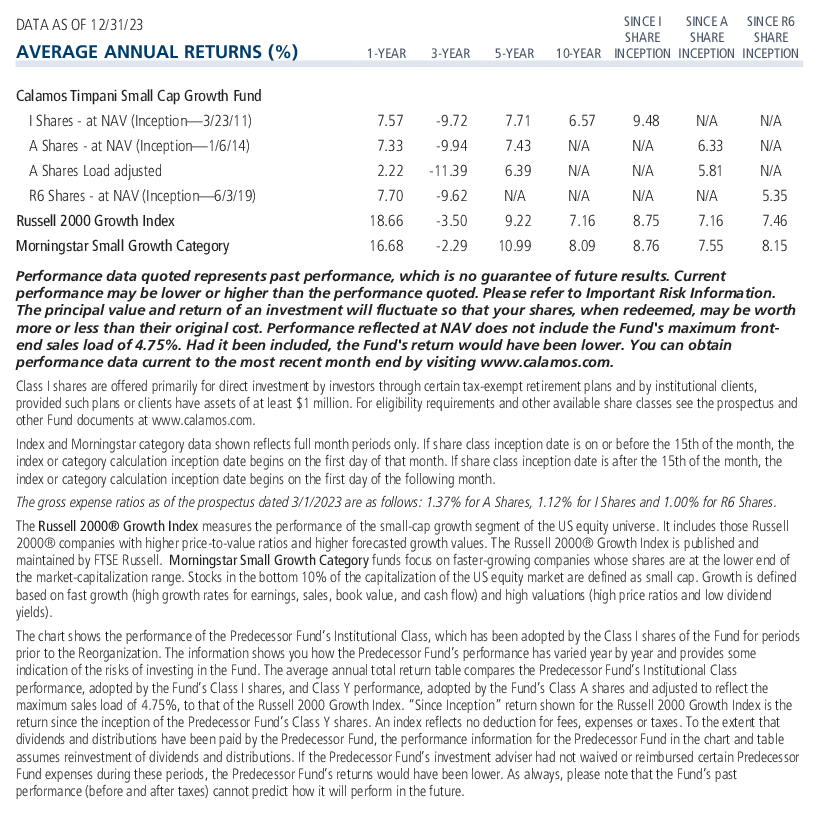

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. Please refer to Important Risk Information and performance information below. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost.

Small cap resurgence: The icing on the cake for Calamos Timpani Small Cap Growth Fund

We believe the most important tailwind for Calamos Timpani Small Cap Growth Fund is an environment that rewards fundamental research and bottom-up security selection. But beyond that, the fund is positioned to benefit from an improved environment for small caps.

-

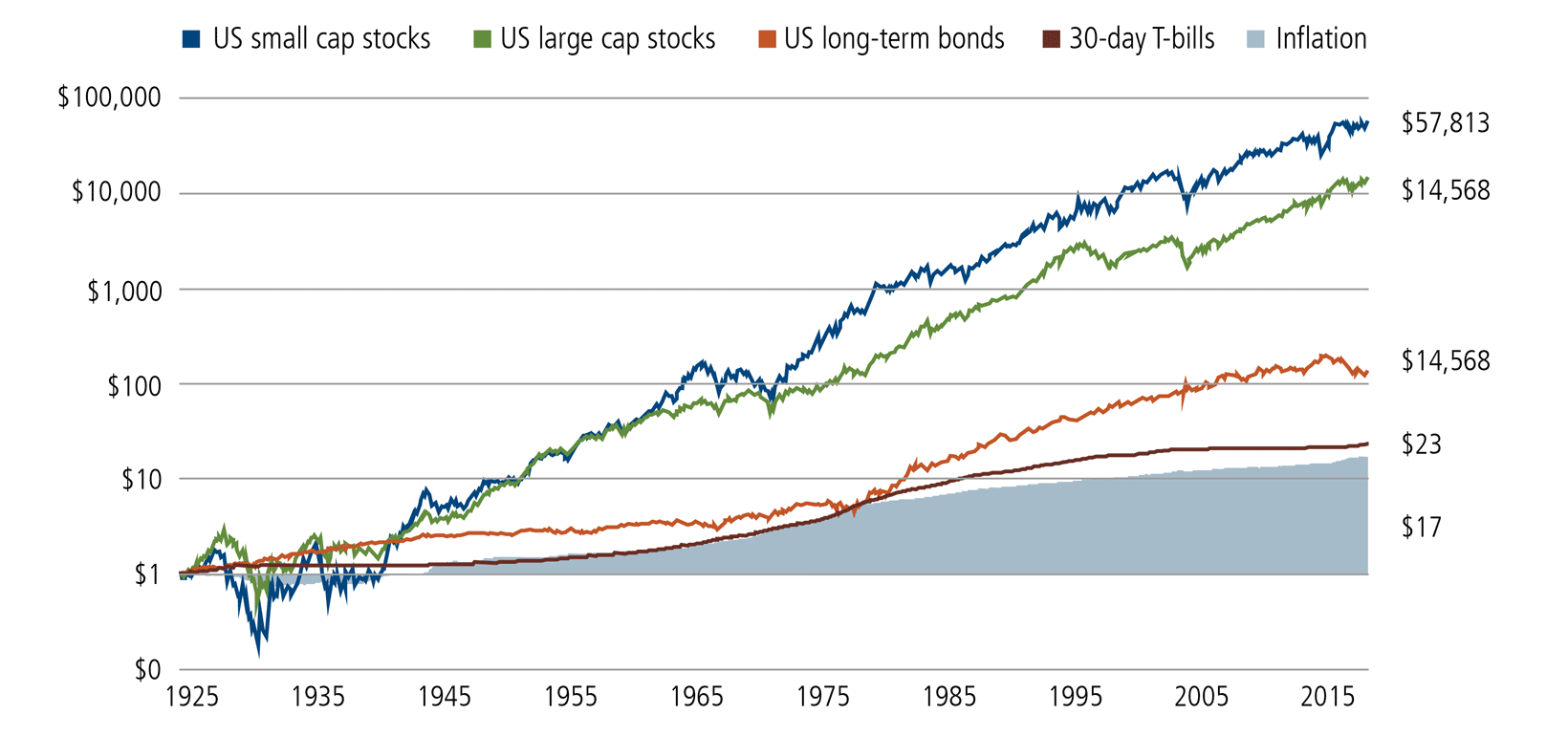

Over the long term, small caps have outperformed large caps

“Reversion to the mean is the iron rule of financial markets,” John Bogle observed—and we agree. Large caps have enjoyed an extended leadership regime, but small caps have delivered stronger performance over the long term.

Small cap stocks have won over time, 1926-2023

Hypothetical growth of $1

Past performance is no guarantee of future results. Source: Morningstar Direct using Ibbotson Associates® and SSBI® indexes. December 31, 1925 to December 31, 2023. See below for additional index definitions.

-

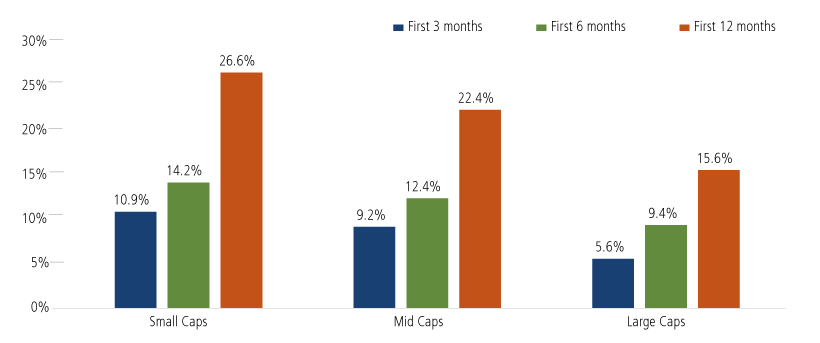

Historically, small caps have benefited most from interest rate cuts

Even if we can’t predict how many times or exactly when the Fed will begin cutting interest rates, we do expect cuts in 2024. Historically, after the Fed’s first rate cut, stocks across the market cap spectrum have rallied, with small caps gaining exponentially.

Small caps have gained the most when the Fed has cut rates

Performance after first rate cut

Past performance is no guarantee of future results. Source: Jefferies using Federal Reserve Board, Haver Analytics, Center for Research in Securities Prices (CRSP®), and the University of Chicago Booth School of Business. Note: used fed funds rate from 1954 until 1963, then used the discount rate from 1963 until 1994 and the fed funds rate after that. Market caps defined by CRSP based on placing market caps into deciles. Deciles 1 and 2 are large, and 6 through 8 are small.

-

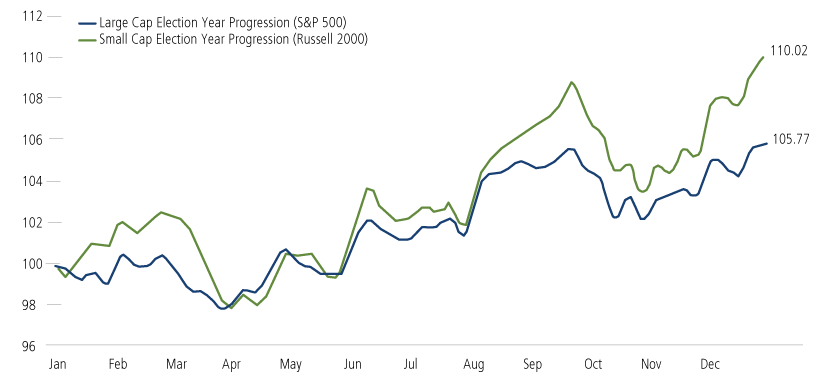

In election years, small caps have outperformed

Although we expect political and fiscal policy uncertainty to fuel volatility in the markets, data going back more than 40 years shows that stocks have performed well in election years, with small caps leading large.

Small caps have beaten large caps in presidential election years

Historical comparison of annual seasonality, 1980‒2020

Past performance is no guarantee of future results. Source: Piper Sandler Technical Research/Bloomberg.

-

Small caps offer better earnings growth prospects

Estimates for small company earnings growth currently outpace large caps, and we believe our team’s proprietary research identifies the most compelling opportunities within this universe. In this recent round of earnings announcements, small companies are giving investors plenty to cheer about, with a higher percentage of small caps beating earnings estimates versus large caps.

CTSIX has established a wide lead versus peers in 2024

Total returns as of 2/15/2024

Past performance is no guarantee of future results. Source: BofA Equity & Quant Strategy, Fact Set

-

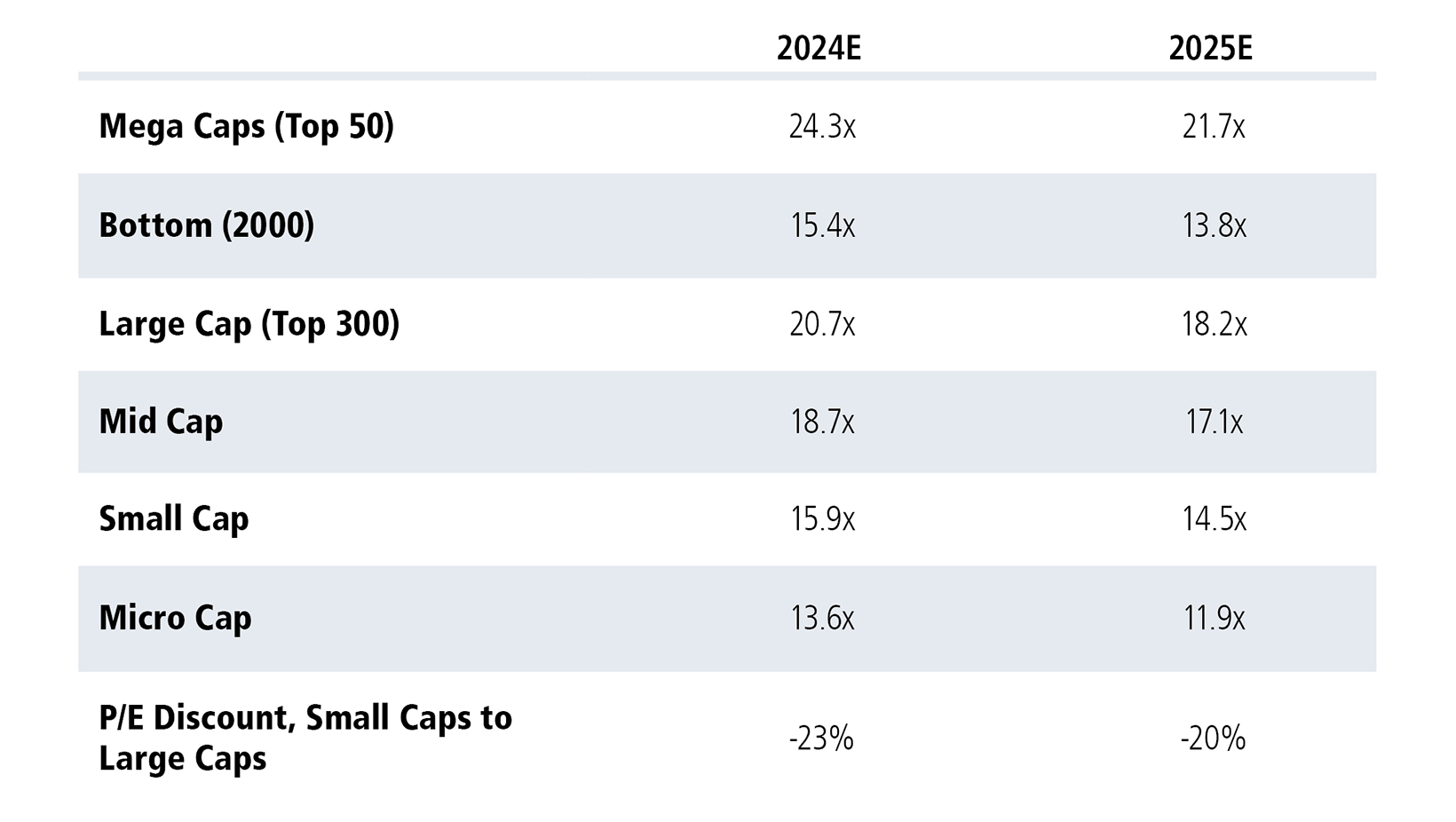

Small caps are attractively valued relative to large caps

Many small cap companies are trading at attractive prices in absolute terms and compared to large caps. Relative valuations are even more attractive for micro caps.

Opportunity for small caps: Valuations

Past performance is no guarantee of future results. Source: The Leuthold Group. January 31, 2024. *A measure of the degree to which the price/earnings ratios of small caps are greater or less than those of large caps. A negative value, or discount, indicates that price/earnings ratios of small caps are less than those of large caps. Price/earnings ratios measure the price of a stock relative to its earnings per share.

Implications for asset allocation

Historically, when small cap stocks have taken off, the tide has turned quickly. After a lengthy large-cap leadership regime, many investors find themselves under-allocated to small cap growth stocks and sidelined from potential upside. In a market where we see fundamentals mattering more and tailwinds for small caps gathering force, we believe Calamos Timpani Small Cap Growth Fund provides a timely choice for enhancing diversification through a time-tested and disciplined approach. Moreover, a nimble asset base enhances the fund’s ability to participate meaningfully in micro-cap opportunities.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund's prospectus.

The principal risks of investing in the Calamos Timpani Small Cap Growth Fund include: equity securities risk consisting of market prices declining in general, growth stock risk consisting of potential increased volatility due to securities trading at higher multiples, and portfolio selection risk. The Fund invests in small capitalization companies, which are often more volatile and less liquid than investments in larger companies. As a result of political or economic instability in foreign countries, there can be special risks associated with investing in foreign securities, including fluctuations in currency exchange rates, increased price volatility and difficulty obtaining information. In addition, emerging markets may present additional risk due to potential for greater economic and political instability in less developed countries.

Indexes are unmanaged, do not include fees or expenses and are not available for direct investment. The S&P 600 Small Cap Index is a measure of US small cap stock market performance. The S&P 500 Index is a measure of US large cap stock market performance. The Russell 2000 Index is a measure of small cap stock performance.

Source: Morningstar Direct. "SBBI" stands for "Stocks, Bonds. Bills, and Inflation". “Stocks, Bonds, Bills, and Inflation”, “SBBI”, and "Ibbotson" (when used in conjunction with a series or publication name) are registered trademarks of Morningstar, Inc. All rights reserved. Used with permission. The IA SBBI US 30-Day Treasury Bill Index measures the performance of U.S. Treasury bills (T-bills) with a maturity of approximately 30 days. The IA SBBI US Inflation Index tracks the historical inflation rate in the United States. It measures the percentage increase in consumer prices over time, reflecting the general rise in the cost of living. ©Morningstar and Ibbotson Associates.

900088 0224