Investment Ideas Home Page

Structured Protection ETFs – The “Double Dip” Trade and Buying Beyond Day One

July 9, 2024

Regarding Calamos’ Structured Protection ETFs, investors often invest right at launch. The combination of equity upside to a cap and 100% downside protection over a defined period is appealing to many investors. We offer another compelling entry point – the “double dip” trade.

The Set Up

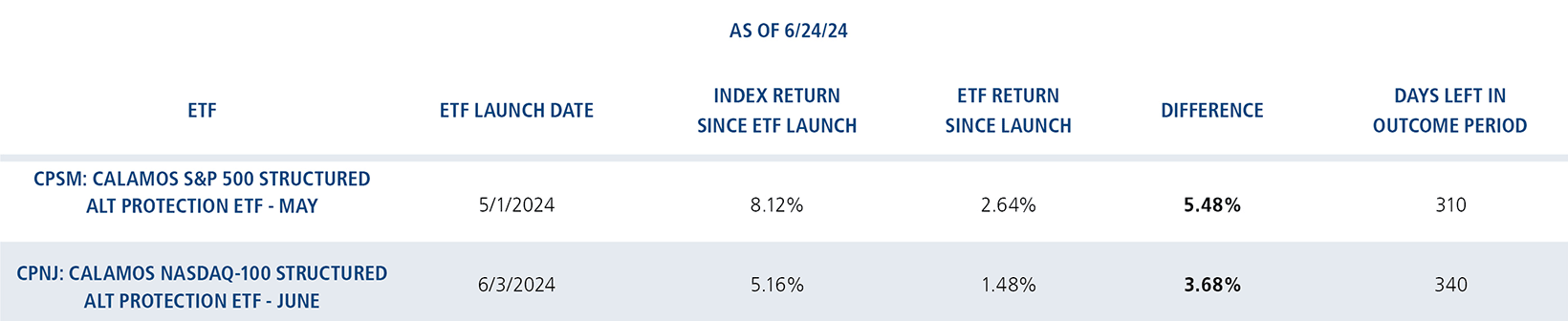

When the underlying index appreciates early in the outcome period, the ETF will appreciate as well. However, as the index and ETF appreciate, investors’ upside cap and downside protection level will also change accordingly (ie: both the upside cap and downside protection level will be lower than they were initially). We’ve seen this early on with both CPSM and CPNJ:

Source: Calamos website. Cap and protection levels are for each Fund’s respective full outcome period as of 6/24/2024.

That brings up an important question: Did investors miss the buying opportunity if they didn’t buy on day one? For certain investors, the answer is a resounding no. In fact, for investors looking to reduce risk from the underlying index or "full equity" exposure, it's arguably an even better trade. Enter the “double dip” scenario.

The “Double-Dip” Trade

When the reference index appreciates early on, a capital-protected ETF won’t move in lockstep initially. Why? Because there’s still premium left in the ETF’s underlying options. For example, as of June 24, 2024, the price return of the S&P 500 is +8.12%, while the return of CPSM is +2.64% since the start of the outcome period.

What happens to the 5.48% return difference? If the market stays flat or appreciates, it won’t be lost! The performance gap will steadily close as the influence of the option premiums decay and the intrinsic value of the options takes over. In other words, investors will still earn that return difference if the market stays where it was or moves higher over the rest of the outcome period.

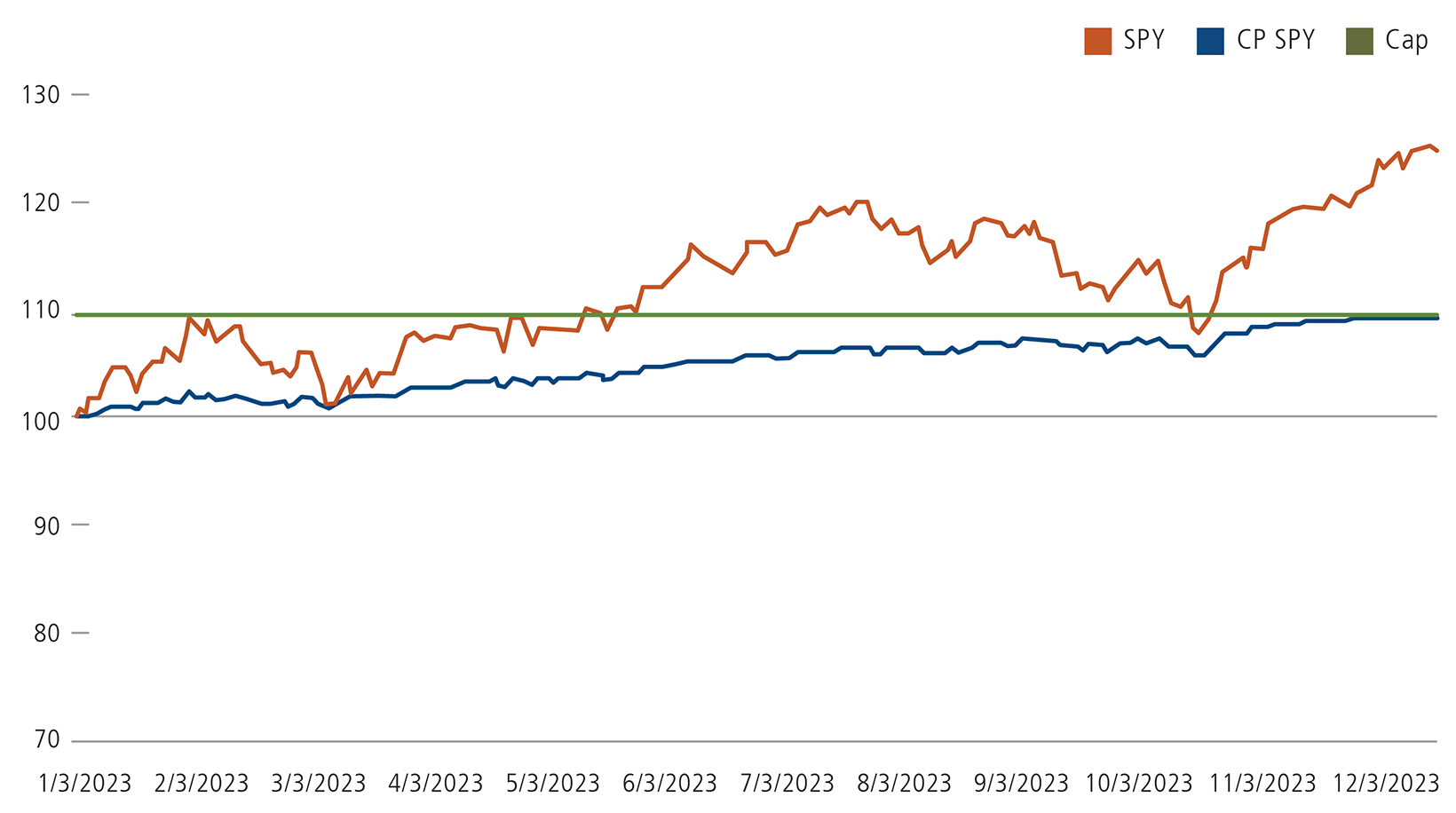

A great example of this over a full one-year outcome period can be seen by looking at hypothetical performance in 2023 using the Merqube Capital Protected US Large Cap Index, which mimics the returns of the SPDR S&P 500 ETF (SPY) up to a “cap”, while having 100% downside protection for every 1-year period.

Year in Review - 2023

Source: MerQube Indices, as of 1/3/23 – 12/31/23, https://merqube.com/index/MQU1PP01. CPSPY is The MerQube Capital Protected US Large Cap Index – January Index (MQU1PP01) is an unmanaged index measuring the value of a “capital protected” equity strategy, tracking upside participation in the returns of the SPDR S&P 500 ETF (SPY) until a “cap”that is at least 1% for every 1 year. Unmanaged index returns assume reinvestment of any and all distributions and, unlike fund returns, do not reflect fees, expenses or sales charges. Investors cannot invest directly in an index. Past performance is no guarantee of future results. The performance of the MerQube Capital Protected US Large Cap Index should not be used as a proxy for the Calamos Structured Protection ETFs.

- Early in the year, SPY reached the upside cap of the Merqube Capital Protected US Large Cap Index, and then exceeded the cap by mid-year.

- The Merqube Index lagged throughout this period, but eventually closed the gap at the end of the outcome period.

The slow decay of option premium and the closure of that return gap over time creates an intriguing entry point. If an investor held SPY, he or she would have realized the full return of 8.12%. By then selling and rotating into an instrument that hasn't yet realized the full move (but might), investors have the possibility to "double dip".

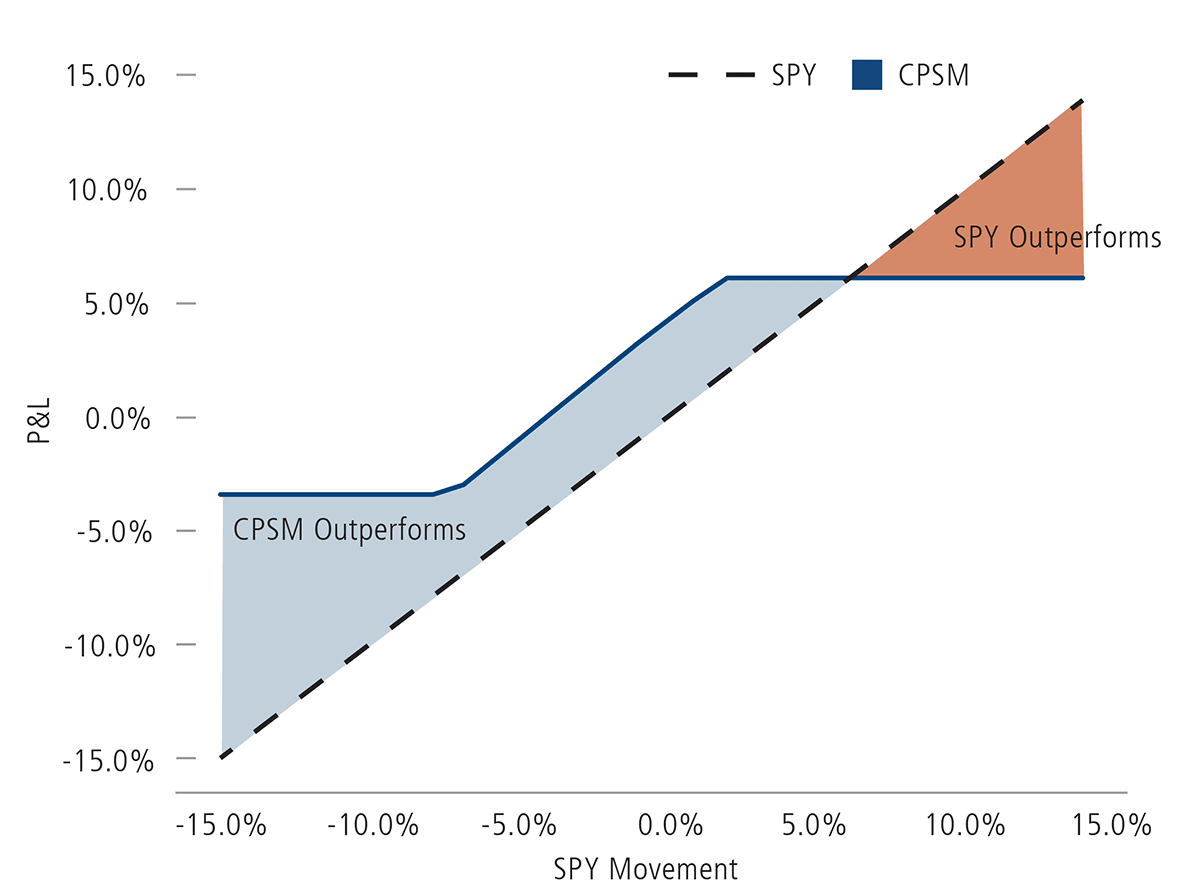

As a result of the gap closing over the course of the outcome period, investors who purchased on 6/24 will not only outperform the underlying index in any down or sideways market, but also on the upside up to an approximate 6% return of SPY. For investors looking to pare risk, this sets up as a very compelling trade.

CPSM vs SPY P&L

Source: Calamos Investments

For more information on our Structured Protection ETFs, visit Calamos Structured Protection ETFs.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund's prospectus.

Investing involves risks. Loss of principal is possible. The Funds face numerous market trading risks, including authorized participation concentration risk, cap change risk, capital protection risk, capped upside risk, cash holdings risk, clearing member default risk, correlation risk, derivatives risk, equity securities risk, investment timing risk, large-capitalization investing risk, liquidity risk, market maker risk, market risk, non-diversification risk, options risk, premium-discount risk, secondary market trading risk, sector risk, tax risk, trading issues risk, underlying ETF risk and valuation risk. For a detailed list of fund risks see the prospectus.

There are no assurances the Fund will be successful in providing the sought-after protection. The outcomes that the Fund seeks to provide may only be realized if you are holding shares on the first day of the Outcome Period and continue to hold them on the last day of the Outcome Period, approximately one year. There is no guarantee that the Outcomes for an Outcome Period will be realized or that the Fund will achieve its investment objective. If the Outcome Period has begun and the Underlying ETF has increased in value, any appreciation of the Fund by virtue of increases in the Underlying ETF since the commencement of the Outcome Period will not be protected by the sought-after protection, and an investor could experience losses until the Underlying ETF returns to the original price at the commencement of the Outcome Period. Fund shareholders are subject to an upside return cap (the "Cap") that represents the maximum percentage return an investor can achieve from an investment in the funds' for the Outcome Period, before fees and expenses. If the Outcome Period has begun and the Fund has increased in value to a level near to the Cap, an investor purchasing at that price has little or no ability to achieve gains but remains vulnerable to downside risks. Additionally, the Cap may rise or fall from one Outcome Period to the next. The Cap, and the Fund's position relative to it, should be considered before investing in the Fund. The Fund's website, www.calamos.com, provides important Fund information as well information relating to the potential outcomes of an investment in a Fund on a daily basis.

These Funds are designed to provide point-to-point exposure to the price return of the Reference Asset via a basket of Flex Options. As a result, the ETFs are not expected to move directly in line with the Reference Asset during the interim period.

Investors purchasing shares after an outcome period has begun may experience very different results than fund's investment objective. Initial outcome periods are approximately 1-year beginning on the fund's inception date. Following the initial outcome period, each subsequent outcome period will begin on the first day of the month the fund was incepted. After the conclusion of an outcome period, another will begin.

FLEX Options Risk The Fund will utilize FLEX Options issued and guaranteed for settlement by the Options Clearing Corporation (OCC). In the unlikely event that the OCC becomes insolvent or is otherwise unable to meet its settlement obligations, the Fund could suffer significant losses. Additionally, FLEX Options may be less liquid than standard options. In a less liquid market for the FLEX Options, the Fund may have difficulty closing out certain FLEX Options positions at desired times and prices. The values of FLEX Options do not increase or decrease at the same rate as the reference asset and may vary due to factors other than the price of reference asset.

Shares are bought and sold at market price, not net asset value (NAV), and are not individually redeemable from the fund. NAV represents the value of each share's portion of the fund's underlying assets and cash at the end of the trading day. Market price returns reflect the midpoint of the bid/ask spread as of the close of trading on the exchange where fund shares are listed.

100% capital protection is over a one-year period before fees and expenses. All caps are pre-determined.

Cap Range – Maximum percentage return an investor can achieve from an investment in the Fund if held over the Outcome Period. Cap range depicted is the high and low cap rate over the past 15 trading days. Actual cap delivered by the Fund may be different.

Protection Level – Amount of protection the Fund is designed to achieve over the Days Remaining.

Outcome Period – Number of days in the Outcome Period.

Nasdaq® and Nasdaq-100 are registered trademarks of Nasdaq, Inc. (which with its affiliates is referred to as the “Corporations”) and are licensed for use by Calamos Advisors LLC. The Fund has not been passed on by the Corporations as to their legality or suitability. The Fund is not issued, endorsed, sold, or promoted by the Corporations. The Corporations make no warranties and bear no liability with respect to the Fund(s).

STRUCTURED ALT PROTECTION ETF and STRUCTURED PROTECTION ETF are trademarks of Calamos Investments LLC.