Investment Team Voices Home Page

Investment Team Voices Home Page

Calamos Fixed Income Suite: Moving in a More Defensive Direction

July 5, 2024

Calamos High Income Opportunities Fund (CIHYX), Calamos Total Return Bond Fund (CTRIX), Calamos Short-Term Bond Fund (CSTIX)

Matt Freund, CFA, Christian Brobst, and Chuck Carmody, CFA

Summary Points:

- We are prepared for softer economic growth, although the stability of corporate credit fundamentals during the quarter indicates that there may be a path for the economy to avoid recession.

- We agree with the Fed’s conclusion that current policy is restrictive, with the remaining question being just how restrictive.

- We continue to migrate portfolio credit quality higher across the Calamos fixed-income funds.

The long-awaited economic slowdown has yet to arrive, and the US consumer continues to outshine the rest of the economic world. Why and how is this happening again? For one, the pie of consumption is growing as the US population expands. Overall, however, believe the strength of the US consumer largely reflects the lingering impacts of Covid aid and the lower sensitivity of US households to interest rates. For example, approximately 95% of the US mortgage market is fixed rate, significantly higher than any other developed economy. This contributes to longer and more variable lags we see domestically, particularly in tightening cycles. As interest rates have been suppressed since the Great Financial Crisis, the lag may indeed take an especially long time to transmit to real economic activity.

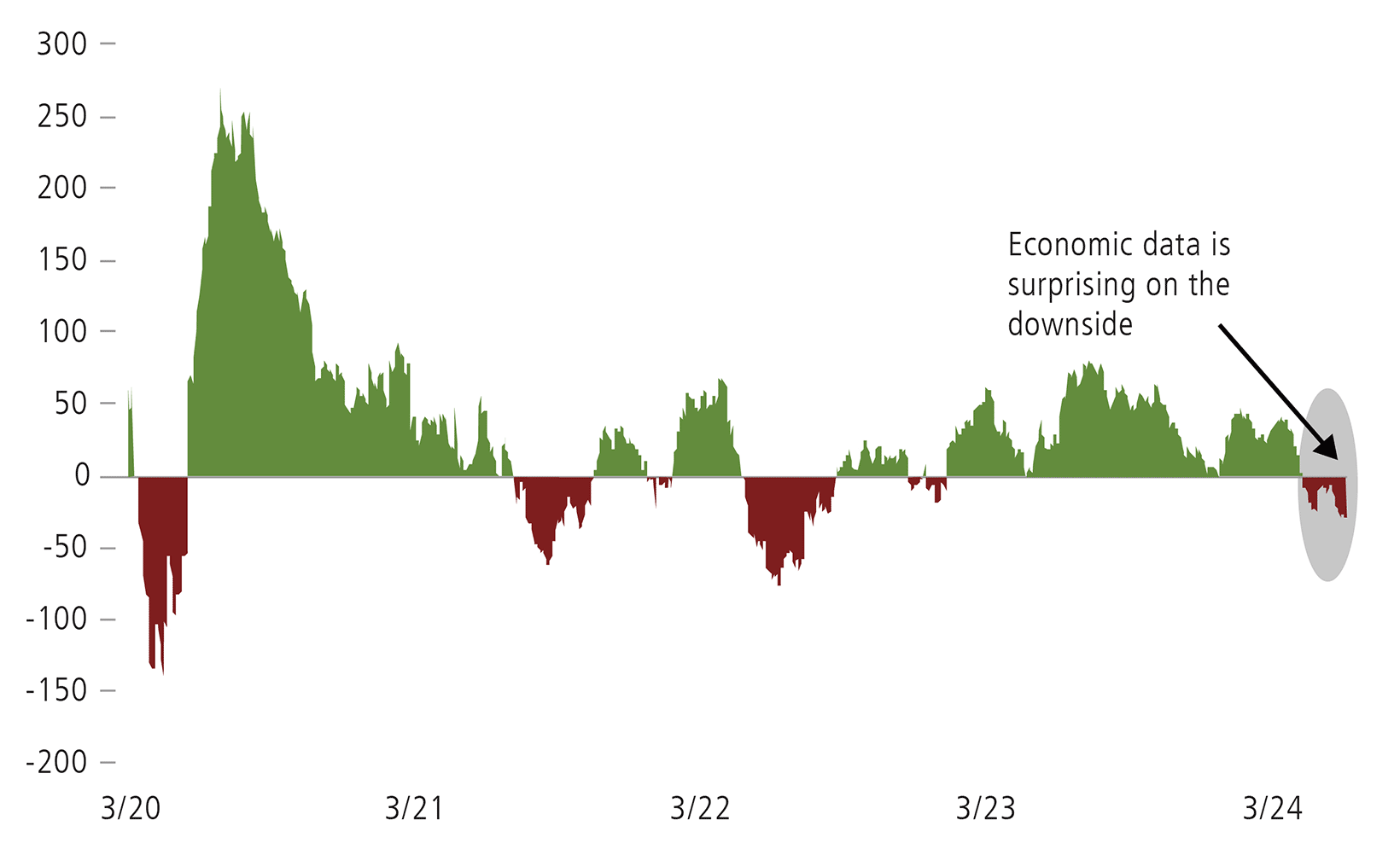

Even so, we see signs of slower domestic economic conditions emerging. Last quarter, we highlighted that the Citigroup Economic Surprise Index showed that growth, activity, and labor measures have been broadly outpacing economist expectations, with an impressive string of beats stretching back to early 2023. However, the direction changed in the second quarter, as data has generally missed economists’ estimates over recent months.

Change for the Worse: US Economic Data is Coming Short of Expectations

Citi Economic Surprise Index, United States

Source: Bloomberg. The Citi Economic Surprise Indices measure data surprises relative to market expectations. A positive reading means that data releases have been stronger than expected, and a negative reading means that data releases have been worse than expected.

Although more balanced, labor market conditions remain an area of strength. Jobless claims and unemployment statistics have been surprisingly stable, and May’s small business survey reported the most bullish hiring expectations in half a year. The establishment survey is moderating but still above the rate necessary to keep up with population growth.

Fed members seem to be getting less certain about the rate path forward. Ranges of possible outcomes cited in the infamous “dot-plot” for 2024, 2025, and the longer-run neutral rate are broadening. This reflects uncertainty among committee members regarding how the neutral rate of interest can be determined in a post-Covid economy. Although inflation has faded (especially for goods producers), service providers and homeowners still have pricing power. The May inflation report supported expectations for Fed cuts in short order, but it is only one data point. The Fed insists it will need to see more progress and a sustainable trajectory back to its 2% inflation goal before embarking on a reversal of the historic tightening cycle of recent years.

At the same time, projections for further rate hikes have been stifled directly by the Fed, and market participants are waiting for data to become convincing enough for the first cut to overnight benchmark rates since 2020. A sudden, unforeseen weakening of activity, labor conditions, or liquidity that requires the Fed to take more aggressive easing action is always possible, but few data points suggest we are headed in that direction. The consumer has shown some signs of weakness, as evidenced by slumping retail sales and rising delinquencies on consumer debt, but levels are similar to 2019. Corporate fundamentals stabilized during the quarter after a two-year-long trend of deteriorating leverage and coverage metrics.

For its part, the market has taken the Fed at its word. Additional hikes are off the table, and the race to front-run the Fed’s rate cuts is underway, with the market currently pricing in two cuts by year-end.

Positioning Implications

Futures markets are pricing in six rate cuts before year-end 2025. Given the resilience of growth and labor metrics, we continue to believe this represents binary outcomes. If the economy achieves a soft landing, six cuts will be too many. If the Fed has miscalculated and something breaks, six cuts are unlikely to be enough. We also believe the market expects too low of a terminal rate. Traditionally, when markets anticipate more rate cuts than we believe possible, we position the funds with durations shorter than those of their benchmarks. That is the case for Calamos Total Return Bond Fund and Calamos High Income Opportunities Fund, although interest rate sensitivity in the high-yield market is a smaller driver of risk and return. However, our expectation for a steeper curve where short maturities benefit from Fed easing and long rates are stickier at higher levels has led us to position Calamos Short-Term Bond Fund with a duration slightly longer than its benchmark.

The stability of corporate credit fundamentals during the quarter indicates that there may be a path for the economy to avoid recession. Although our team expects the default rate in the high-yield market to continue to increase to its long-term average, we also expect large performance differences between winners and losers. We continue to position portfolios with more corporate debt exposure than their benchmarks as our fundamental research process continues to identify high-yield issuers and industries where investors are well compensated for the current risk profile. However, given the compressed credit spread environment across security types, we are migrating portfolio credit quality higher across the Calamos fixed income funds as we prepare for softer growth going forward.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

Diversification and asset allocation do not guarantee a profit or protect against a loss. Alternative strategies entail added risks and may not be appropriate for all investors. Indexes are unmanaged, not available for direct investment and do not include fees and expenses.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be appropriate for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

Duration is a measure of interest rate risk. Dovish refers to accommodative monetary policy.

The establishment survey is a monthly survey of approximately 119,000 businesses and government agencies representing approximately 629,000 worksites throughout the United States.

Important Risk Information. An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund’s prospectus.

The principal risks of investing the Calamos Total Return Bond Fund include: interest rate risk consisting of loss of value for income securities as interest rates rise, credit risk consisting of the risk of the borrower missing payments, high yield risk, liquidity risk, mortgage-related and other asset-backed securities risk, including extension risk and portfolio selection risk.

The principal risks of investing in the Calamos High Income Opportunities Fund include: high yield risk consisting of increased credit and liquidity risks, convertible securities risk consisting of the potential for a decline in value during periods of rising interest rates and the risk of the borrower to miss payments, synthetic convertible instruments risk, interest rate risk, credit risk, liquidity risk, portfolio selection risk and foreign securities risk. The Fund’s fixed income securities are subject to interest rate risk. If rates increase, the value of the Fund’s investments generally declines. Owning a bond fund is not the same as directly owning fixed income securities. If the market moves, losses will occur instantaneously, and there will be no ability to hold a bond to maturity.

The principal risks of investing in the Calamos Short-Term Bond Fund include: interest rate risk consisting of loss of value for income securities as interest rates rise, credit risk consisting of the risk of the borrower to miss payments, high yield risk, liquidity risk, mortgage-related and other asset-back securities risk, including extension risk and prepayment risk, US Government security risk, foreign securities risk, non-US Government obligation risk and portfolio selection risk.

900229 0624