Investment Team Voices Home Page

Investment Team Voices Home Page

Finding Much to Like in Global Equity Markets

July 5, 2024

Nick Niziolek, CFA, Dennis Cogan, CFA, Paul Ryndak, CFA, and Kyle Ruge, CFA

Summary Points:

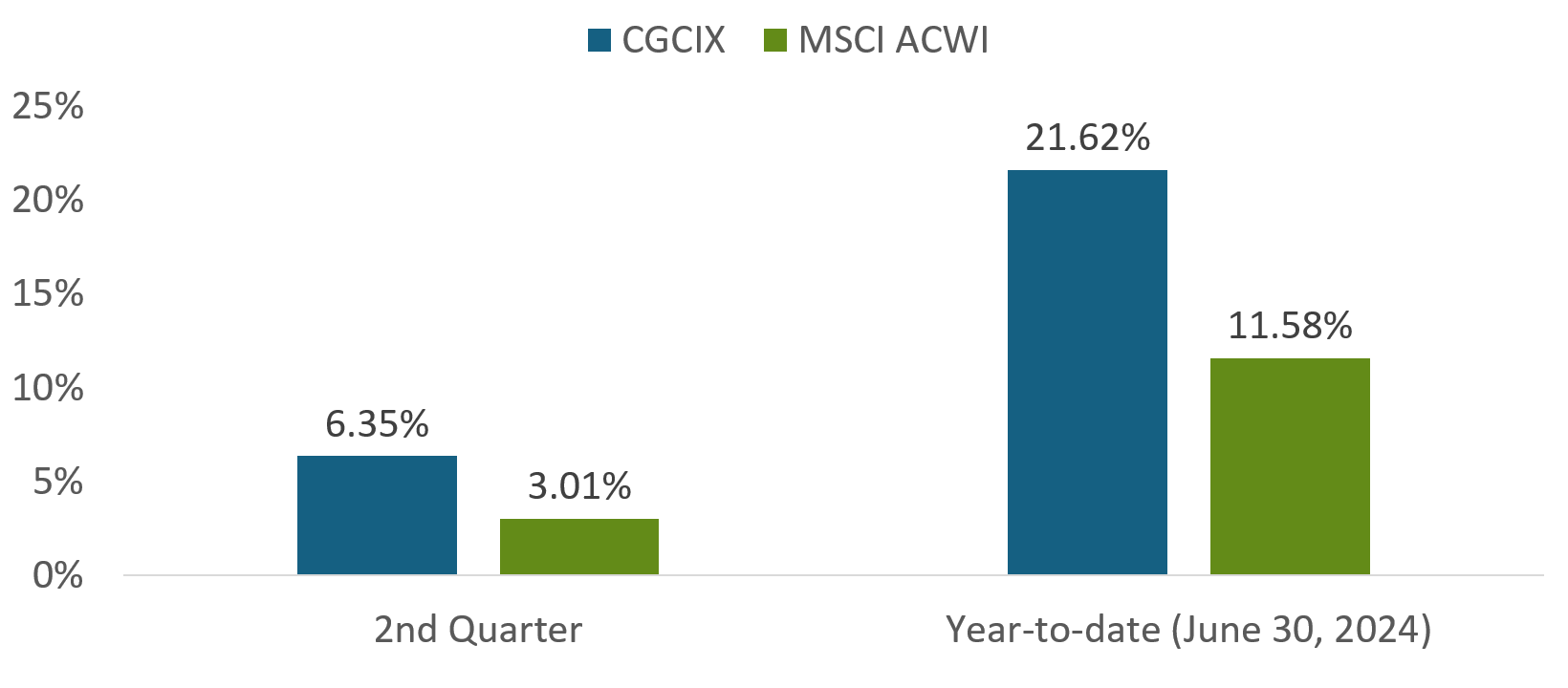

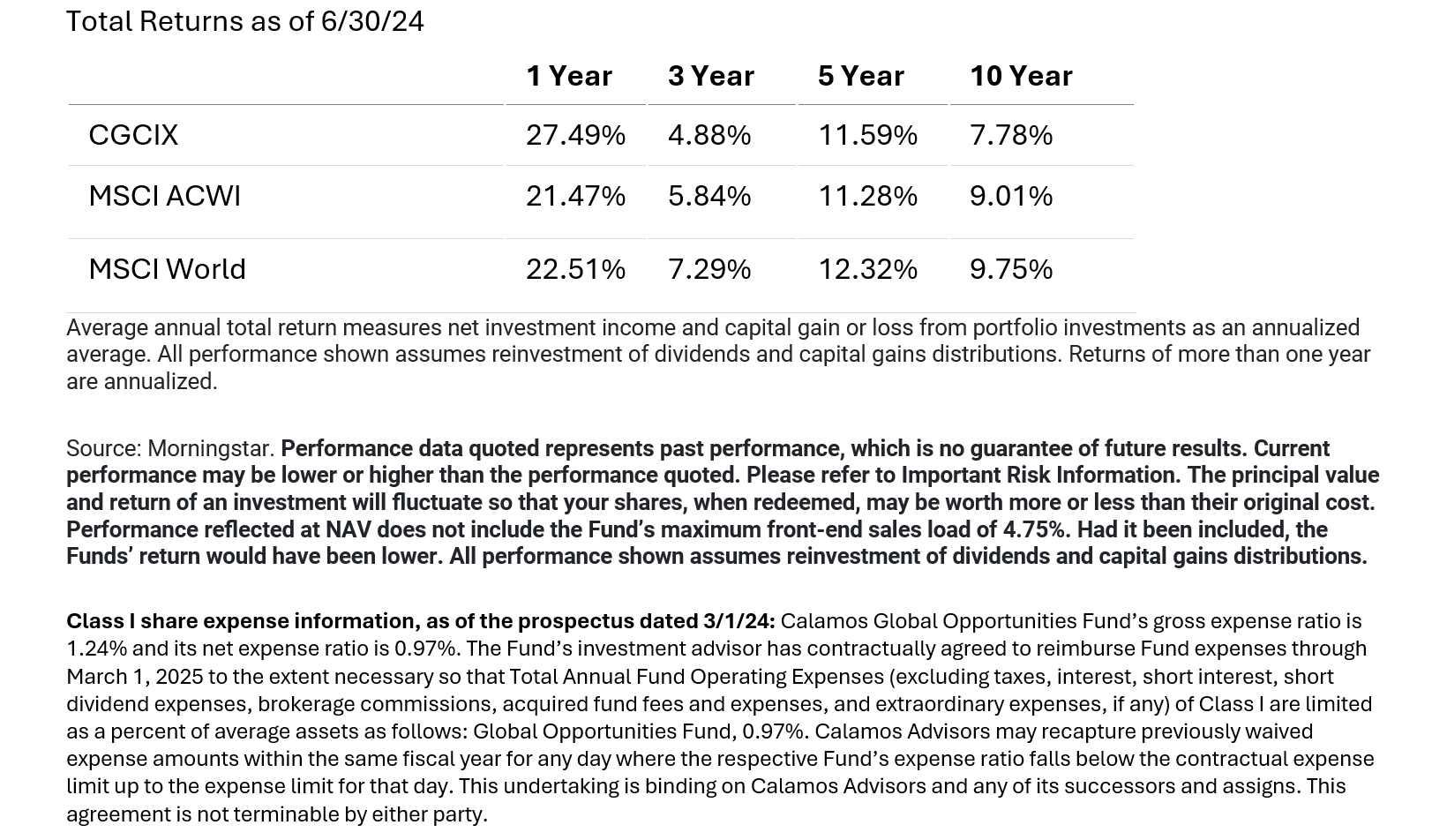

- Calamos Global Opportunities Fund’s returns for the quarter and year-to-date exceeded those of its benchmark.

- CGCIX positioning aligns with our view that the economy is in a disinflationary growth market cycle regime.

- This environment favors growth equities, including those positioned to benefit from secular growth themes.

- We invest opportunistically in convertible securities as a way to enhance risk/reward skew, and have identified a growing number of opportunities within the emerging markets.

Global equity markets added to year-to-date gains during the second quarter, even though economic data regarding the growth and inflation outlook remained mixed. Peak Covid re-opening tailwinds and peaks in inflation and accelerating growth are all in the rearview mirror for most major economies. Even so, we believe the global economy is resilient overall, and recession is not our base case. Regarding our macro framework, we believe we are in a period of disinflationary growth characterized by decreasing inflation and decent economic fundamentals, which is a generally benign backdrop and an ideal environment for growth equities, including those with secular tailwinds.

Calamos Global Opportunities Fund Has Performed Strongly in 2024

Source: Morningstar.

Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. Please refer to Important Risk Information. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance reflected at NAV does not include the Fund’s maximum front-end sales load of 4.75%. Had it been included, the Fund’s return would have been lower. All performance shown assumes reinvestment of dividends and capital gains distributions. As of the prospectus dated 3/1/2024, CGCIX’s gross expense ratio is 1.24%.

Below, we highlight some key positioning themes in Calamos Global Opportunities Fund:

US Markets: More to Cheer than Just the Mag 7

Although Calamos Global Opportunities Fund is modestly underweight to the US versus the MSCI ACWI Index, US companies are the fund’s largest country weighting as of June 30, 2024. The disinflationary growth narrative certainly appears to be in force in the US: Some recent economic data and indicators have weakened, but overall growth remains solid, and inflation continues to fall. This creates a favorable backdrop for companies benefiting from strong and sustainable growth, including those at the center of powerful secular growth themes. Our investment process is focused on finding the best of these. Secular growth has been a driver of the market’s strong year-to-date performance, and CGCIX has been positioned for these tailwinds as well.

One of the most common concerns—or even complaints! —that investors are voicing these days relates to the concentration of the market’s returns in a small number of stocks, most often— the “Magnificent Seven. ” We find this a little confusing. Consider the Russell 1000 Index. Although on a market-cap-weighted basis, it is true that a relatively small number of companies have driven a large portion of the Index’s year-to-date return, it’s also true that more than 100 names have returned more than 25% year-to-date. These performers represent a variety of industries, market caps, and growth themes. For active managers who are willing and able to express conviction, we believe there will continue to be many opportunities to invest in companies that the market will reward for their strong fundamentals and ability to grow their intrinsic values. And this is only in the US; globally, the opportunity set is even greater!

Japan: Targeting Pockets of Opportunity

For more on CGCIX:

The Best Kept Secret in Global Investing

The Three Pillars of Calamos Global Opportunities Fund

Identifying Global Growth Opportunities Through a Thematic LensJapan counts among our top five country weightings as of the end of the quarter. We recently returned from a research trip to Japan, which included company tours, meetings with senior management teams, and spirited debates and discussions with some of our peers. Although the tone from company management teams was generally optimistic and investor interest in Japanese equities is high, we are mindful of changing sentiment within the domestic economy. In 2023, we were struck by how the average worker was cheering inflation—and the significant wage gains inflation fueled. However, the realization that inflation is eroding purchasing power is sinking in. This new reality is likely to have knock-on effects on consumer-driven sectors of the economy.

Consequently, although the combination of valuations, improved corporate governance, and a focus on optimizing capital allocation supports our optimistic view of Japan’s equity market, we have emphasized global companies domiciled in Japan because these multinationals can also benefit from the continued unfolding of the global capex cycle.

Another cause for optimism within the Japanese equity market centers on the success of recent retirement savings reforms, which have led to increased investments in local and overseas markets. New savings plans create a steady flow of capital from the retail segment into the capital markets and have also increased the average person’s interest in the markets. We believe this higher engagement will help drive additional reforms and incentivize companies to be shareholder-friendly.

The Opportunity of EM Convertible Securities

We use convertible securities opportunistically to improve the fund’s risk/reward skew. Convertibles allow us to capture equity market upside with potentially less downside exposure, providing an attractive way to access growth opportunities. Over recent quarters, we have increased our exposure to emerging market convertibles. We have built exposure to attractive businesses by investing in convertible structures that are less volatile than their underlying equities while still providing exposure to the stock market’s upside.

During the second quarter, several large Chinese internet companies issued convertible bonds to fund stock buybacks, and their management teams communicated to the market that they believed the underlying equities were significantly undervalued. In several cases, we also had a favorable view of valuations and invested in these newly issued convertibles to participate in well-priced access to growth.

Industrials: A Closer Look

Our exposure to the industrial sector is multi-dimensional, spanning secular, turnaround/capital improvement, and more cyclical names. Reflecting the sector’s breadth of opportunity, the fund includes a meaningful overweight to industrials. The secular opportunities for data center infrastructure are among the most exciting for the sector. Both power and thermal equipment will see an uptick in demand because AI chips and servers use three to four times more electrical power than traditional central processing units. According to the IEA, global data center total electricity consumption is expected to double from 2022 to 2026.

As overall electricity consumption rises, new infrastructure investments will be made inside data centers (e.g., new servers, cooling equipment, and additional power supplies) and outside the centers to expand power generation and transmission to meet demand.

Our overweight also reflects the bottom-up fundamentals in many industrial companies, including improved operational efficiencies, margins, and cash flows; and new management teams committed to strengthening competitive positioning. Japan-domiciled companies are well represented within our industrial holdings, where country-specific factors provide new catalysts for management teams to improve operational efficiencies, eliminate noncore holdings, and return capital to shareholders—a welcome shift after years of stagnant corporate evolution.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

Indexes are unmanaged, do not include fees or expenses and are not available for direct investment. The MSCI World Index measures the performance of stocks from developed markets, and the MSCI ACWI Index measures the performance of stocks from developed and emerging markets.

Diversification and asset allocation do not guarantee a profit or protect against a loss. Alternative strategies entail added risks and may not be appropriate for all investors. Indexes are unmanaged, not available for direct investment and do not include fees and expenses.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be appropriate for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

Important Risk Information. An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund’s prospectus.

Foreign security risk: As a result of political or economic instability in foreign countries, there can be special risks associated with investing in foreign securities, including fluctuations in currency exchange rates, increased price volatility and difficulty obtaining information. In addition, emerging markets may present

The principal risks of investing in the Calamos Global Opportunities Fund include: convertible securities risk consisting of the potential for a decline in value during periods of rising interest rates and the risk of the borrower to miss payments, synthetic convertible instruments risk consisting of fluctuations inconsistent with a convertible security and the risk of components expiring worthless, foreign securities risk, emerging markets risk, equity securities risk, growth stock risk, interest rate risk, credit risk, high yield risk, forward foreign currency contract risk, portfolio selection risk, and liquidity risk.

900236 0624