Investment Team Voices Home Page

Investment Team Voices Home Page

Why We’re Sticking to Quality and Diversification

July 5, 2024

Jim Madden, CFA, Tony Tursich, CFA, and Beth Williamson

Summary Points:

- We’ve seen the equity market narrow once again, led by a handful of high-momentum technology stocks in the AI space.

- Rallies in momentum stocks have often reversed dramatically, exposing investors to significant pain.

- Our time-tested approach continues to focus on long-term returns and downside risk management, leading us to stick to a well-diversified, quality-oriented positioning.

- The fund continues to emphasize attractively valued companies across sectors that are creating shareholder value through innovation and by managing both financial and non-financial risks.

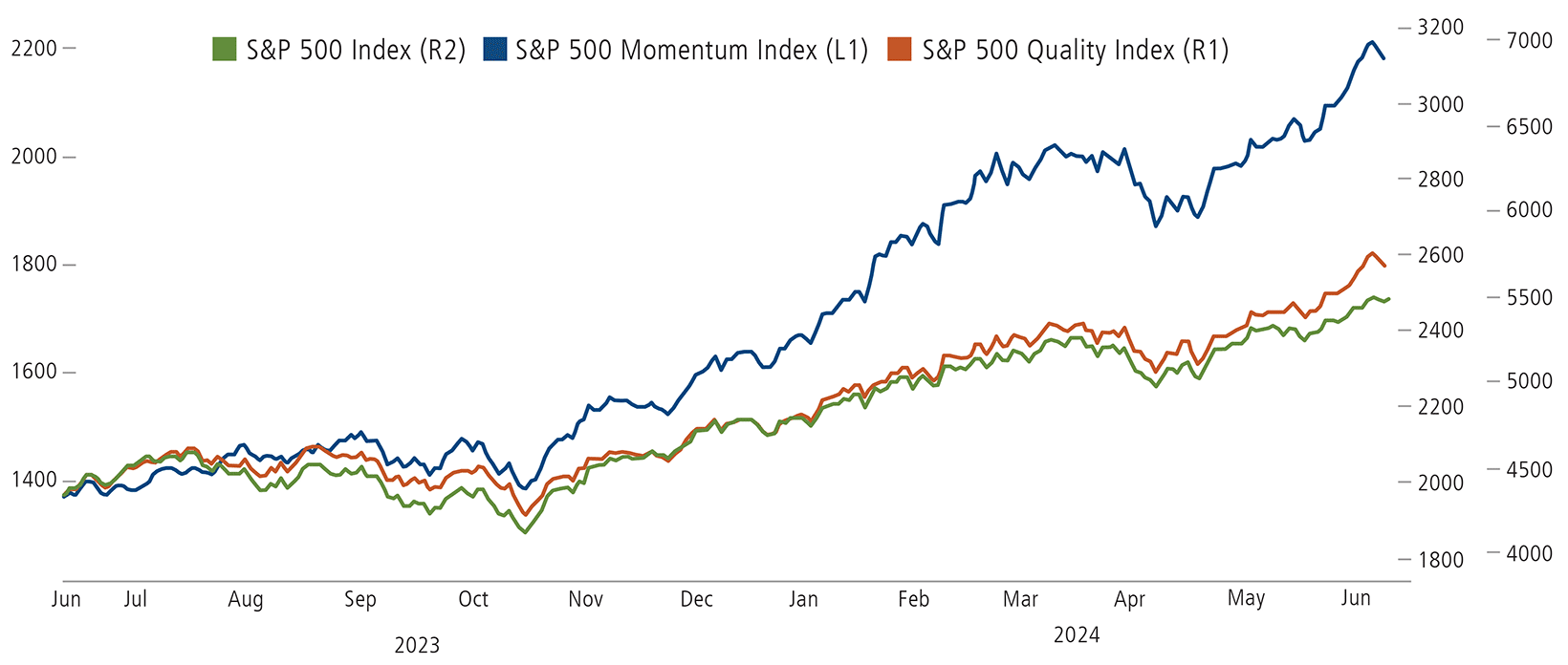

Momentum investing, a strategy of chasing what’s hot and selling what’s not, has been a winning strategy for the past 12 months and certainly year-to-date. Momentum’s outperformance since the artificial intelligence hysteria took hold has been astonishing. The chart compares the performance of high-momentum stocks to the broader equity market and to quality stocks and highlights the magnitude of the current rally.

US Large-Cap Stocks: Momentum Versus Quality

Past performance is no guarantee of future results. Source: Bloomberg.

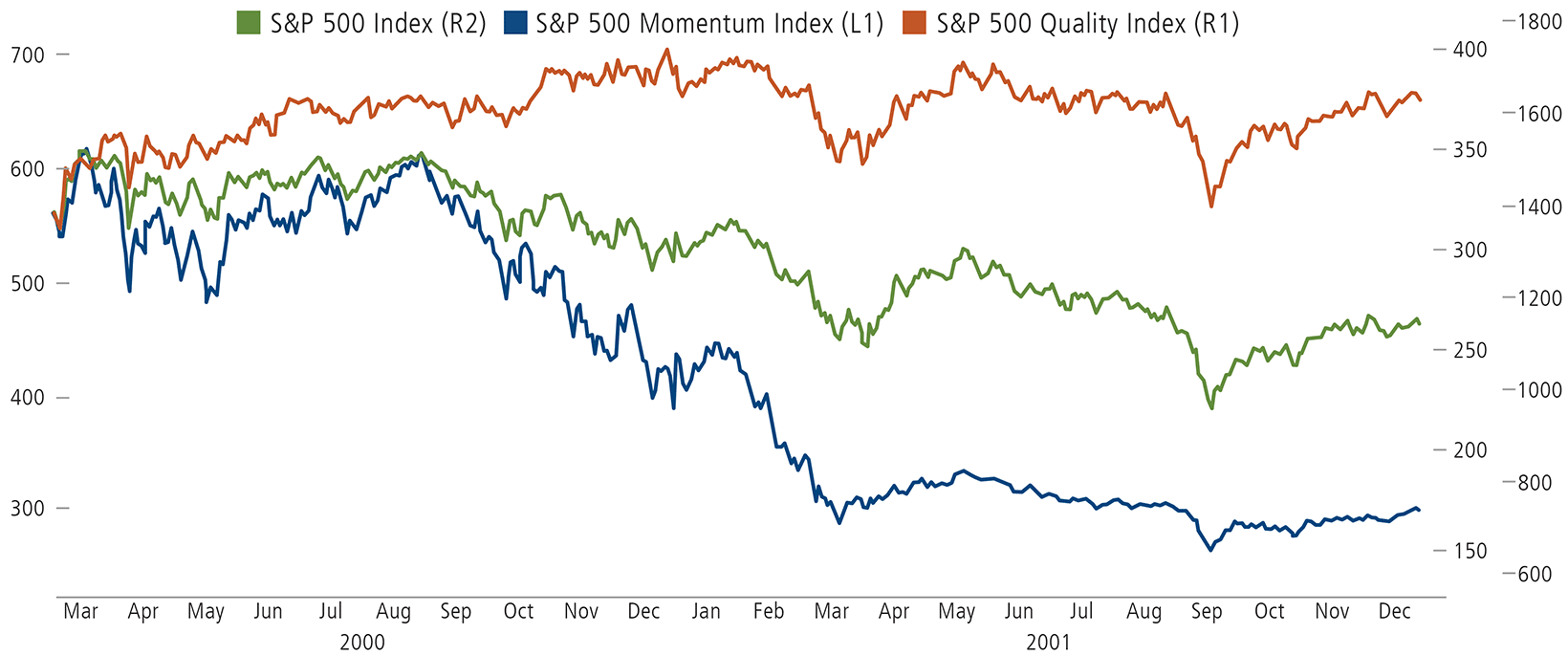

It’s rare for momentum rallies to persist for a long time, and when they reverse, the downturns can be dramatic. Consider the period from the peak of the dot-com bubble in March of 2000 through the end of 2001. Momentum underperformed the broader market significantly, while quality held up quite well. The S&P 500 Quality Index was up 20%, while the S&P 500 Momentum Index was down more than 40%. We may not like these markets, but we are sticking to our quality discipline because we are confident that fundamentals will ultimately prevail.

Case Study of a Momentum Rally Collapse: Dot-com Implosion

Past performance is no guarantee of future results. Source: Bloomberg.

Concentration Risk Versus Diversification Opportunity

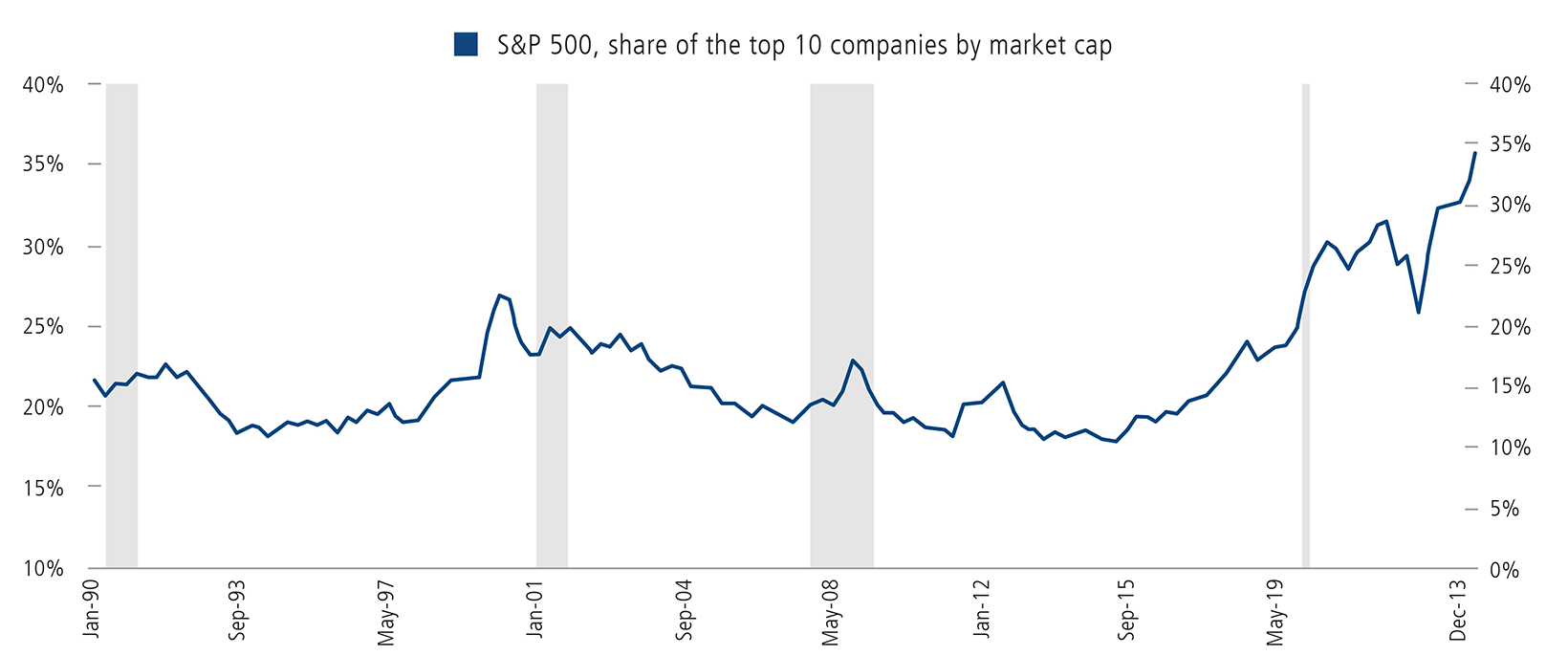

Concentrated investing has also been a winning strategy in 2024. Large-cap stocks have been the clear leader during the current bull market. The top decile of the 50 largest stocks in the S&P 500 Index was the only subsector to have outperformed the broader S&P 500 this year. In fact, five stocks accounted for 60% of the aggregate S&P 500 Index’s year-to-date return. From a market cap standpoint, these five stocks have collectively surged by 35% and now comprise 25% of the S&P 500 Index’s equity capitalization.

Just 10 Companies Comprise More than a Third of the S&P 500’s Overall Market Cap

Recessions are indicated by shaded areas. Past performance is no guarantee of future results. Source: Bloomberg, Apollo Chief Economist.

We don’t believe this narrow leadership will last. In the second half of the year, we expect big tech’s profit growth to slow, opening the door to broader market leadership. Meanwhile, sectors like materials and health care are positioned for significant profit growth in the fourth quarter after contracting in the first.

Decades of experience support our conviction in the value of diversification. Diversification seeks to mitigate unsystematic risk and can lead to better opportunities and more consistent, higher risk-adjusted returns. Accordingly, we have positioned the fund to participate not only in technology growth (including in the AI ecosystem) but also in a breadth of innovation, including more idiosyncratic opportunities. Looking forward, we believe the fund is well positioned to benefit from better relative performance of other economic sectors.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

Diversification and asset allocation do not guarantee a profit or protect against a loss. Alternative strategies entail added risks and may not be appropriate for all investors. Indexes are unmanaged, not available for direct investment and do not include fees and expenses.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be appropriate for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations.

Environmental, social and governance (ESG) s based on the premise of investing in companies that have good environmental records, are ethically run and have a positive social impact.

An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s)will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund’s prospectus.

The principal risks of investing in the Calamos Antetokounmpo Sustainable Equities Fund include: equity securities risk consisting of market prices declining in general, growth stock risk consisting of potential increased volatility due to securities trading at higher multiples, large-capitalization stocks as a group could fall out of favor with the market, small and mid-sized company risk, sector risk, portfolio turnover risk, and portfolio selection risk.

The Fund's ESG policy could cause it to perform differently compared to similar funds that do not have such a policy. The application of the social and environmental standards of Calamos Advisors may affect the Fund's exposure to certain issuers, industries, sectors, and factors that may impact the relative financial performance of the Fund—positively or negatively—depending on whether such investments are in or out of favor.

Calamos Antetokounmpo Asset Management LLC (“CGAM”), an investment adviser registered with the SEC under the Investment Advisers Act of 1940, serves as the Fund’s adviser (“Adviser”). CGAM is jointly owned by Calamos Advisors LLC and Original C Fund, LLC, an entity whose voting rights are wholly owned by Original PE, LLC which, in turn, is wholly owned by Giannis Sina Ugo Antetokounmpo. Giannis Sina Ugo Antetokounmpo is the majority shareholder of Original C, with a 68% ownership interest.

Mr. Antetokounmpo serves on the Adviser’s Board of Directors and has indirect control of half of the Adviser’s Board.

Mr. Antetokounmpo is not a portfolio manager of the Fund and will not be involved in the day-to-day management of the Fund’s investments, and neither Original C nor Mr. Antetokounmpo shall provide any “investment advice” to the Fund. Mr. Antetokounmpo provided input in selecting the initial strategy for the Fund.

Mr. Antetokounmpo will be involved with marketing efforts on behalf of the Adviser.

If Mr. Antetokounmpo is no longer involved with the Fund or the Adviser then “Antetokounmpo” will be removed from the name of the Fund and the Adviser. Further, shareholders would be notified of any change in the name of the Fund or its strategy.

The Adviser is jointly owned and controlled by Calamos Advisors LLC and, indirectly, by Mr. Antetokounmpo, a well-known professional athlete. Unanticipated events, including, without limitation, death, adverse reputational events or business disputes, could result in Mr. Antetokounmpo no longer being associated or involved with the Adviser. Any such event could adversely impact the Fund and result in shareholders experiencing substantial losses.

900233 0624